Change

The best thing about the future is that it comes one day at a time.

– Abraham Lincoln

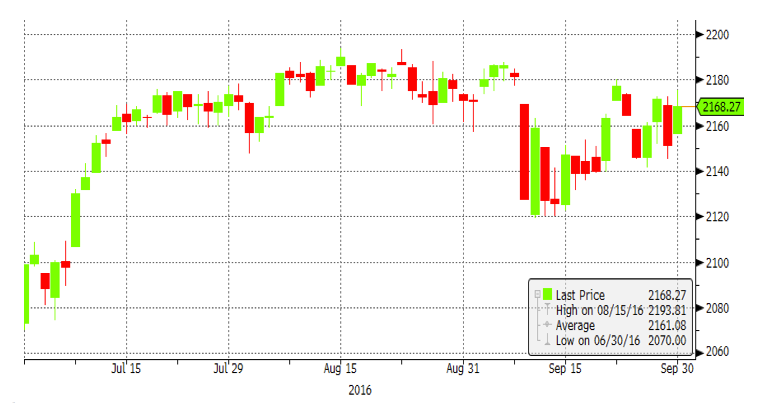

Change is in the air. If you live in the Northern states, change is in the air with cooler temperatures and changing foliage heralding fall’s imminent arrival. Change is also evident in financial markets. After five consecutive positive months, the S&P 500 index finally stalled in August and September, down 0.12% each month. Volatility returned in September (down 2.5% on 9/9 alone).

Figure One: S&P 500, 6/30-9/30/2016

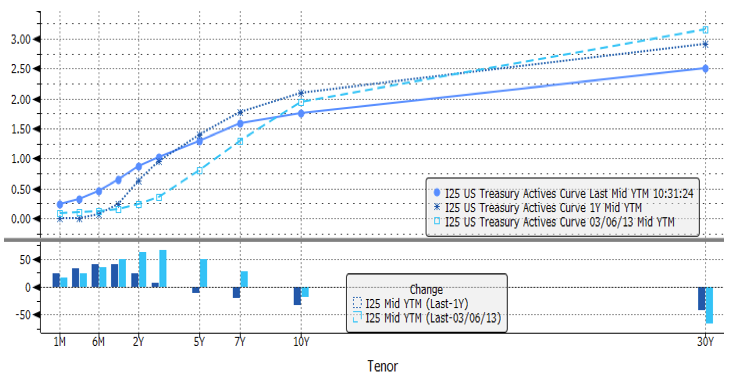

Bond yields are also changing. Having bottomed at 1.36% in early July, the U.S. 10 year note’s yield rose to 1.60% at 9/30/2016 and reached 1.76% on 10/11/2016. The U.S. yield curve has flattened from where it was the last couple of years, as shown below:

Figure Two: U.S. Yield Curve, 2014-10/11/2016

US investment grade bonds rose 0.46% in the third quarter and 6% year-to-date as measured by the Barclays US Aggregate Bond Index. The index is yielding 2%, less than the S&P 500’s 2.2% dividend yield. Although international rates remain even less attractive, their volatility has also risen with rates off their lows. German ten year Bunds vacillated in and out of negative territory in September ending at -0.12%. Even the ten year Japanese bond yield approached zero, yielding -0.007% at 9/12 and closed the quarter at -0.09%, well off their -0.30% in late July.

Stocks rose around the globe last quarter:

all major global stock indices were up with the Hang Seng +12% and Germany’s DAX +8.6% in local currency terms and 4% more when measured in U.S. dollars. The S&P 500 was up 3.3% bringing its year-to-date (YTD) gain to 6.1%; not bad considering it was down 9% in the first three weeks of 2016.

Economic Fundamentals are mixed

Domestically, employment and housing remain steady. Unemployment remains at 5% while average home prices are rising 5%+ a year. Manufacturing continues to show weakness with Industrial Production down 0.4% for August and is down 1.1% over the past year. Retail sales also remain weak and capital spending uninspiring

Valuations are high

Price/earnings multiples for the S&P 500 Index are over 20 times (x) trailing earnings and 16x next twelve months’ estimated earnings – a bit above long term averages but not egregious. We sense there is a lot of cash on the sidelines that could be invested if economic growth and earnings accelerate, but outflows from the stock market could escalate if economic weakness worsens. Investors are also aware of the high likelihood of the US Federal Reserve Bank raising rates in December of 2016 and beyond. The trend in unemployment, inflation, and aggregate demand will likely dictate the timing and slope of rate hikes in the U.S.

Is cash king?

Regency’s investment philosophy is anchored on history, experience, and common sense. Generally, we prefer to be fully invested believing that time in the market has proven to be more effective than timing the market. Our experience recognizes that at times investors can be overly optimistic or pessimistic generating episodic investment opportunities. We look to tilt portfolios accordingly when we are convinced that these opportunities are present. Experience and common sense helps us to see through the noise of headlines and one-off events as we analyze markets objectively.

In this currently unusual world of low to negative yields, we suspect that the transition to a more normal investment environment will be a challenging one. We also recognize that our clients are human and care for more than just maximizing long-term wealth which is evidenced in a recent study by Cambridge University.1 According to the study, people express that a large cash balance in the bank makes them happy – regardless of its prudence or lack thereof. In this sense, cash is “king.” But we need to remember that holding cash for any long period of time guarantees us a loss of purchasing power as long as inflation persists. Currently, inflation is low (1-2%) but cash yields almost nothing. This gap, over time, can be material to making our money last in retirement.

Outlook

Rates will likely remain low, even if the Fed raises its discount rate later this year and treasury yields rise a bit from here. How bond and stock markets transition into higher, but still low rates will likely depend on economic progress domestically and internationally. Uncertainty may continue to feed higher volatility possibly near term ahead of U.S. elections in early November but also into 2017 and beyond. As always, we will interpret events and trends and look for conviction as we strive to protect your hard earned investments entrusted to our care.

As President Lincoln said, “…the future will come one day at a time” but as it does, it will bring change. Change is best dealt with by regularly re-examining our mutual perspectives and expectations and discussing them with you collaboratively. Your customized financial plan reflects your investment risk tolerance and is expressed in a diversified portfolio. We look forward, as always, to discussing any substantive changes in your situation during our regular investment reviews. Thank you for your continued confidence in your Regency team.

Call us with any questions.

Happy Fall!

Andrew M. Aran, CFA

Mark D. Reitsma, CFP®, CMFC

Timothy G. Parker, CFA

Bryan D. Kabot, CFP®, AAMS®

Click here to download a pdf version.

Regency Wealth Management is a SEC Registered Investment Advisor managing over $600 million for families and small institutional investors. Regency was founded in 2004, is headquartered in New Jersey, and serves clients across the country.